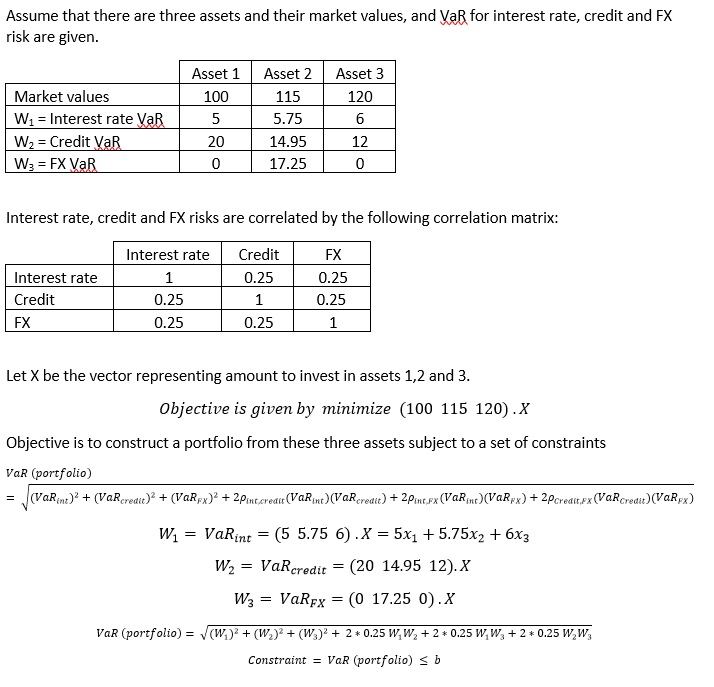

I have a problem similar to Markowitz portfolio optimization that I would like to transform into second-order cone programming. I have a linear objective function with a quadratic constraint (assuming that I can take the square on both sides of the constraint to make it quadratic).

Assume that $X$ is a vector of decision variables. The objective function and the constraint are below. How can I transform it into a second-order cone constraint? \begin{align}\min&\quad c^\top X\\\text{s.t.}&\quad\sqrt{\sum_{i,j}^n(W_i\cdot X)^2+(W_j\cdot X)^2+2\rho_{i,j}(W_i\cdot X)\cdot(W_j\cdot X)}\le b\end{align} where

$W_i$ and $W_j$ are matrices of constant values of the same dimension as $c^\top$

$\rho_{i,j}$ are correlation coefficients, the matrix generated by it can be assumed to be positive semi-definite

$b$ is a constant.

For example, when $n=2$, the constraint is given by $$\sqrt{(W_1\cdot X)^2+(W_2\cdot X)^2+2\rho_{1,2}(W_1\cdot X)\cdot(W_2\cdot X)}\le b.$$

I would like to understand this both when it is expressed in a more compact matrix form and also when written in the more simplified summation form (as in the question).

For example,