Sorry to ask a question about the basic Markowitz portfolio optimization. The example is from Mosek's example book.

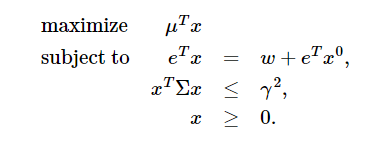

The basic Markowitz portfolio optimization is formulated as:

The book mentioned we can simply remove the constraint $x \ge 0$ to allow short-sell in this formulation.

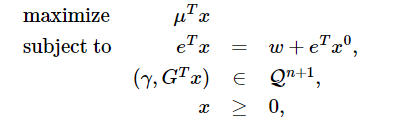

However, my question is about the conic formulation of original problem, which was given as:

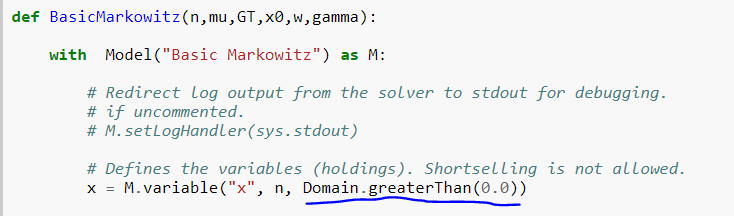

Assuming we similarly remove the constraint $x \ge 0$ in this conic formulation, will it allow short-sell, i.e. $x \lt 0$? My feeling is yes since the cone $Q^{n+1}$ only requires $x_0$ which is $\gamma$ to be non-negative. I tried to change the sample codes below to remove the non-negativity constraint.

But the results seems to be the same. Just would like to confirm if my understanding is correct.

Thank you!