TLDR: When doing sensitivity analysis (speciaficallyspecifically the objective coefficients), there maximum allowable increase and decrease before the solution changes is only valid when a single coefficient changes. Is there a way to generalize when multiple values change?

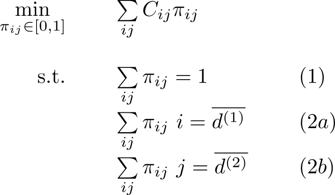

Context: My model (see below) is a simple minimize cost of a weighted sum subject to 2 constraints. The coefficients in my objective are not known well and vary based on some distribution. So I approximate by using the sample mean. So i sample multiple times to get the coefficients subject to some confidence interval. The more I sample, the tighter the interval but each sample is VERY VERY computationally expensive. The cardinality of i and j is at most 6, giving us a maximum of 36 variables. So, I wanted to see if there is stage where given the confidence intervals, I know that the LP solution is unlikely change with additional samples?

My mind first went to sensitivity analysis but the results are only valid when a single parameter changes. But since this is a small problem, is there a way to genaralizegeneralize this further?